Costamare Bulkers - A Boat Load of Special Situations Sailing Under the Radar

Info

This memo was initially written around May 29th, 2025

Business Overview

Costamare Bulkers (CMDB) is a dry bulk shipping company formed via a spin-off from Costamare Inc. (CMRE). It owns 38 vessels and charters 48 more through its CBI (Costamare Bulkers Investments) platform, giving it a combined fleet of 86 ships totaling ~10.8 million DWT. CMDB generates revenue via a mix of spot and time charters, complemented by freight trading and hedging through the CBI platform. The company emphasizes operational flexibility and aims to capitalize on dry bulk market volatility.

Spin-Off Situation

The spin-off aimed to isolate Costamare’s dry bulk business (SpinCo) from its container operations (RemainCo), enabling more transparent performance evaluation. CMDB was recapitalized post-spin with ~$205M in liquidity (cash and funding from RemainCo) and ~$172M in debt, including $85M in forgiven related-party loans. The Konstantakopoulos family, which controls Costamare Inc., took a ~60% stake in CMDB—demonstrating insider alignment and confidence in the new entity.

For those of you who are familiar with special situations - you'll realize this is a spinoff + recap situation.

Current Valuation

2024 Revenue: $1.2 billion

Estimated Book Value: ~$705M (Note that CMDB claims to have a NAV of ~$800M. I have made a few conservative adjustments)

2024 Operating Cash Flow: Negative $55.5M

Market Cap (as of 5/29/2025): $227.76M

P/S Ratio: 0.19

P/B Ratio: 0.32

These standalone numbers mean little without context. Compared to peers in dry bulk shipping:

CMDB trades at a steep discount to peers. The discount likely stems from CMDB's unprofitability and uncertain recovery timeline. Plus, CMDB surely suffers from the selling dynamics triggered by spinoff.

Valuation Scenarios Based on Peer Multiples

Downside (DSX levels):

P/S = 0.72 → $860.4M

P/B = 0.34 → $239.7M

Mid-Range (SHIP/SB/GNK average):

P/S = 1.12 → $1.338B

P/B = 0.49 → $345.5M

Upside (GOGL/SBLK average):

P/S = 1.67 → $1.995B

P/B = 0.85 → $599.3M

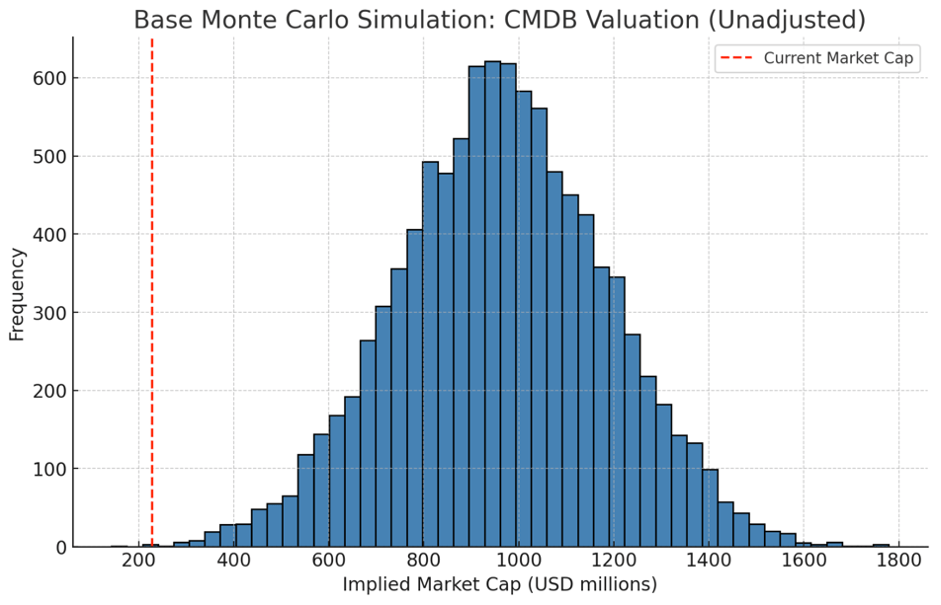

To better understand what this distribution means in aggregate, let’s run a Monte Carlo simulation (10,000 simulations) using peer valuation distributions (P/S mean = 1.12, P/B mean = 0.49). Results are as follows:

Mean: $964M →323% Upside (from $227.76M)

Median: $964M →323% Upside

5th Percentile: $596M →161% Upside

95th Percentile: $1.3B →486% Upside

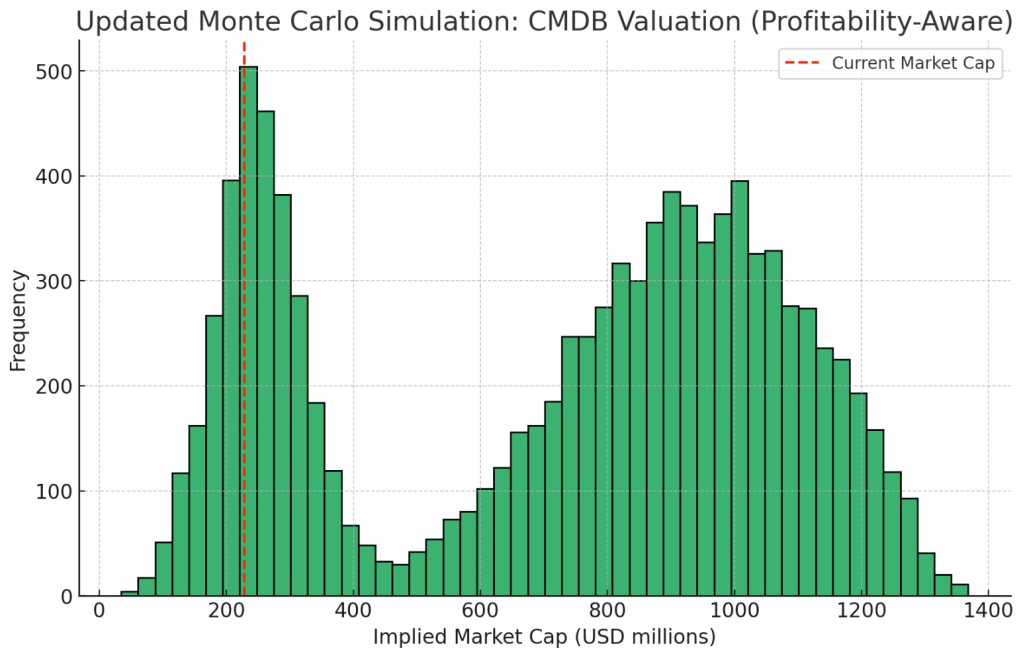

To better reflect CMDB's lack of profitability, an adjusted simulation was run using capped distributions (P/S ≤ 1.5, P/B ≤ 0.6) and a 30% weighting for low-multiple scenarios:

Mean: $721M →216% Upside (from $227.76M)

Median: $818M →259% Upside

5th Percentile: $185M →19% Downside

95th Percentile: $1.2B →427% Upside

The result is a bimodal distribution: one peak (left) representing CMDB remaining distressed, and another (right) assuming operational improvements. Even in poor outcomes, downside is limited—heads I win, tails I don’t lose much.

Investment Thesis

CMDB offers asymmetric upside due to:

Spin-off Dynamics: As Joel Greenblatt noted, spin-offs often result in mispricing. CMDB share price has declined since the spin, likely due to forced selling and limited coverage.

Conservative Balance Sheet: $160M in cash vs. $172M in debt post-spin.

Cyclicality Tailwind: Dry bulk is in a downcycle—any rebound in rates could sharply improve cash flow and sentiment.

The core assumption is CMDB must return to cash flow breakeven. Its clean balance sheet, refocused mandate, and scale give it a fair chance.

Risks

Management Quality: The Costamare family has a mixed track record; CMRE stock has stagnated over the past decade. Their control of SpinCo is a concern.

Cash Burn: Persistent operating losses could erode equity value if market conditions remain weak.

Macro Headwinds: Recession or trade slowdowns could weigh on shipping demand. However, CMDB’s focus on raw materials mitigates exposure to consumer trade shocks.

Conclusion

CMDB is a classic cigar-butt, spin-off special situation. Despite valid execution risks, its deeply discounted valuation, strong insider alignment, and potential operational catalysts create a compelling opportunity for contrarian investors. Downside appears contained; upside is substantial if execution improves.

Sources: CMDB IR Presentation, SEC Filings.

Disclaimer:

The information provided in this content is for informational and educational purposes only and should not be construed as financial or investment advice. The opinions expressed are those of the author and do not constitute a recommendation to buy or sell any securities or financial instruments. While efforts are made to ensure accuracy, the information may become outdated or incomplete over time. Investing involves risk, including the potential loss of principal. Always conduct your own research or consult with a licensed financial advisor before making any investment decisions. The author may hold positions in the securities discussed.