Dino Polska - the Walmart of Eastern Europe?

Info

This memo was initially written around January 31st, 2025

A Dino store has everything you need, nothing more.

Dino Polska (Dino) is a discount retailer chain based in Poland. Dino offers basic staples, like bread, vegetables, fruits, and fresh meat alongside non-food everyday items like detergent. As a discount retailer, Dino aims to be the most affordable and convenient grocery market in its vicinity.

Dino achieves affordability by adopting a pure-play strategy focused on rural and suburban locations, avoiding competitive urban markets. This approach targets a homogenous consumer base, simplifying inventory and supply chain with an SKU count of around 5,000. Additionally, Dino builds and owns every store to save on rent long-term and keeps each store layout identical, maximizing repeatability, accelerating operational learning curves, and lowering building costs. Their vertically-integrated meat processing plants enable them to perfectly coordinate a supply of affordable fresh meat with minimal spoilage rates.

For convenience, Dino employs a small store format of 400 sq meters, designed to serve about 2,500 residents. This decentralized network of stores allows them to be located within walking or cycling distance to customers while remaining economically viable even in remote towns with only a few thousand residents.

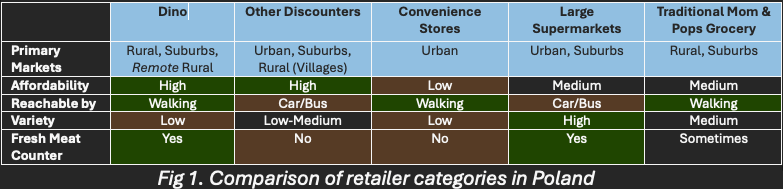

Fresh meat counters are valued for their perceived quality in Polish cuisine, which emphasizes chicken and pork. Most Polish discount groceries lack fresh meat (and offer packaged meats) due to coordination challenges in preventing spoilage while keeping costs low.

The combination of small store format and offering products at a good value keeps Dino highly competitive against its discounter peers, as shown in the comparison below:

Dino’s track record speaks for itself. Since its founding in 1999, it has grown into a $7 billion revenue business in 2024 with more than two thousand stores across western and central Poland. Dino’s net income has also grown at a CAGR of 35% in the last 10 years with an ROIC above 20% since 2018.

Dino has one clear competitive moat and a less tangible one.

Counter position: Dino’s strategy of focusing on rural areas with low-density populations is a core aspect of its small store format model. In contrast, Dino’s main competitors like Biedronka and Lidl struggle to expand into rural areas due to differing customer preferences and spending power. Urban and rural customers have distinct tastes, necessitating either a reduction in product variety or increased inventory in distribution centers to meet diverse demands. By avoiding urban markets, Dino perfects its unit economics in rural areas, whereas competitors can only achieve this balance by risking their overall operating margin. In short, major retailers with existing city presence have limited staying power in villages.

Brand power: Dino's brand power is evident through social media discussions among Polish residents, who often regard Dino as a quality retailer despite its low costs. For instance, Dino's fresh meat counter is highly praised, as Poles consume a lot of meat and associate a traditional meat counter with quality. In contrast, Biedronka, which only offers packaged meat, struggles to maintain this perception of freshness.

Another strength of Dino’s brand is its straightforward approach to customer service. During recent price wars among discount retailers, competitors offered complex daily bundles that, while seemingly cheap, were purposefully designed to be confusing to customers. Some Poles perceived these marketing strategies as deceptive. However, Dino's daily offers are clear and simple, such as "buy X bundle for Y price today," which fosters greater trust and satisfaction among customers.

The company’s management team has demonstrated good track record and is highly incentivized to produce adequate long-term shareholder returns.

Extremely high insider ownership: the founder, Tomasz Biernacki, owns about 51% of the outstanding shares, without a dual class share structure.

Stellar track record: Dino has consistently generated good and increasing returns on invested capital (ROIC) since 2014, ranging from 16% to 25%. Since 2018, ROIC exceeded 20%. For a capital-heavy, real-estate heavy business model, achieving 20%+ ROIC is quite impressive and would be impossible without a tight control on costs and disciplined capital allocation.

Rational capital allocation: historically, the management team has not paid dividend or repurchased shares. Dino has focused on investing in new stores and distribution centers to capture new markets. Given its ability to maintain high ROIC, it’s clear that these reinvestments have good incremental returns.

Here are some risk factors that can negatively impact investment results:

Real estate costs: Dino’s expansion model heavily relies on acquiring land. If real estate prices were to appreciate significantly, this can reduce new store’s ROI.

Intensified competition: If Lidl, Biedronka, or other competitor successfully replicates Dino’s small store / rural model, Dino can face much greater headwind.

Growth stagnation: Although Dino still has significant room for growth in Poland (mainly eastern regions), the remaining whitespace is not infinite. Sooner or later, international expansion would be needed to maintain its current trajectory.

War: Poland can face significant disruptions due to nearby conflicts (Ukraine, Russia) or an outright invasion by Russia. The implications would be disastrous.

Given Dino’s current market valuation (enterprise value) of $11 billion, I estimate the long-term expected return on investment to be around 6% to 11% per year. Despite Dino’s excellent business qualities and growth prospects, current valuation (price to free cashflow of >100x) assumes Dino to achieve very high growth rate in the next decade. High expectations is a source of downside risk if valuation turns pessimistic.

Disclaimer:

The information provided in this content is for informational and educational purposes only and should not be construed as financial or investment advice. The opinions expressed are those of the author and do not constitute a recommendation to buy or sell any securities or financial instruments. While efforts are made to ensure accuracy, the information may become outdated or incomplete over time. Investing involves risk, including the potential loss of principal. Always conduct your own research or consult with a licensed financial advisor before making any investment decisions. The author may hold positions in the securities discussed.