Lessons From the Greatest and Their Greatest Mistakes

A story about brilliance, collapse, and survival

Bill Miller’s career is one of the most instructive arcs in modern investing because it contains all three acts: a historic rise, a public collapse, and a credible redemption. At Legg Mason Value Trust, Miller became a legend by beating the S&P 500 for 15 consecutive years. Then came 2008, Miller decided to bet heavily in financial stocks during the panic, but these companies did not recover and some went bust. This mistake devastated his fund, losing roughly 70% of its value and destroying much of the prestige he had built over decades. For years since his departure from Legg Mason, most investors on Wall St would remember him as the man who flew too high and took too much risk—flying too close to the sun guaranteed his failure.

For many investors, that would have been the end. It was not. Miller rebuilt his career through Miller Value Partners, continued to benefit from some of his most important long-term holdings, and later made an early investment in bitcoin that became one of the defining wins of his second act. That is why his career is so worth studying. It is not useful because it is clean or flattering in hindsight. It is useful because it contains all three lessons at once: how distinctive thinking can drive extraordinary success, how the wrong kind of risk can overwhelm even a great investor, and how a serious setback can force a deeper understanding of markets, risk, and survival.

Focus on the Roots, Not the Branches

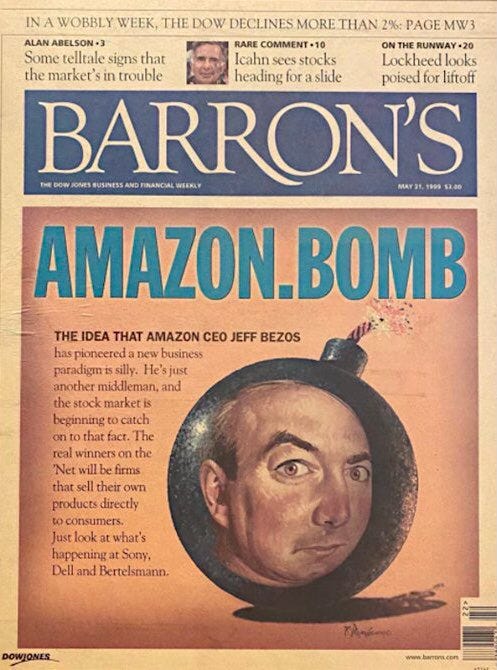

The first lesson comes from Miller’s rise: he saw businesses through multiple lenses, not just financial screens. The best example is Amazon. In May 1999, Barron’s ran its now-infamous “Amazon.bomb” cover story, arguing that investors were only beginning to realize how many problems the company had. By conventional value standards, Amazon looked completely wrong. It was not statistically cheap, its future was highly uncertain, and many people doubted it would survive. Miller leaned in anyway. His fund became the third-largest Amazon shareholder, behind only Jeff Bezos and MacKenzie Scott. In a 2001 Fortune profile, Miller recalled meeting Amazon executives at the Santa Fe Institute in 1999 and coming away deeply impressed by the company’s economic model. He saw a business that could achieve major economies of scale, avoid the burden of physical retail inventory, and operate with a structurally lower cost base. More importantly, he believed Amazon had the potential to become a winner-take-most business rather than a conventional near-term earnings story. His timing was poor, since he bought near the peak of the dot-com bubble, but the underlying thesis was extraordinarily right.

That instinct helps explain why Miller outperformed for so long. He did not think investing was about buying the lowest multiple on a spreadsheet. He tried to understand a business the way you might understand a person: its character, its incentives, its resilience, and what it could become over time. Much of his work was a form of future-casting. He would ask where the company might be five or ten years out, then work backward to judge whether the business had the quality to survive the path in between. This is what made him look like a maverick. He was often buying what others rejected, not because he simply enjoyed being different, but because he was focused on underlying circumstance rather than surface attributes. Michael Mauboussin captured this distinction well when he described Miller as a circumstance-based investor rather than an attribute-based one.

Onlookers often describe the investment strategy of successful investors as eclectic. Perhaps it is more accurate to describe their approach as circumstance-based, not attribute-based. Bill Miller is a good case in point. Miller’s approach is decidedly circumstance based, yet he is routinely criticized for straying from an attribute-based mindset

Michael Mauboussin

That mindset was reinforced by two important influences outside traditional finance. One was philosophy, which trained Miller to question assumptions, hold competing ideas in tension, and distinguish reality from convention. The other was his long involvement with the Santa Fe Institute, where complexity theory offered a richer view of markets and businesses as adaptive systems with many interacting parts, feedback loops, and occasional regime shifts. From that perspective, value is not simply “cheap on a multiple.” It is the gap between what the market believes is happening now and what the business may actually become. Miller’s first lesson, then, is that great investing often comes from seeing the deeper structure of a business before the numbers fully reveal it. The investor who only studies static attributes may miss what the company is in the process of becoming.

Anything Multiplied by Zero is Still Zero

The second lesson comes from Miller’s fall, and it is harsher: even a great investor can be destroyed by the wrong type of risk. His collapse in 2008 was not a normal drawdown where earnings weaken and valuations compress. It was a systemic crisis in which the market stopped asking what a company was worth over time and started asking whether it could survive next week. Miller moved decisively into “ground zero” of part of the financial meltdown and loaded up on distressed financial companies such as Bear Stearns, AIG, and Citigroup. This was consistent with an instinct that had worked for him before. When fear becomes extreme, bargains appear. But in 2008, many of these stocks were not simply misunderstood assets. They were highly levered institutions facing a true liquidity and solvency problem. These companies can move from cheap bargains to worthless in days.

Miller’s own reflection is unusually blunt…

The thing I didn’t do from day one was properly assess the severity of this liquidity crisis. I was naive.

Bill Miller reflecting on his 2008 experience

That is the key point. He did not merely get a valuation wrong. He misidentified the nature of the event. A systemic liquidity crisis is not a normal market dislocation. It changes the rules of the game. When funding disappears and confidence breaks, intrinsic value can become temporarily irrelevant because survival becomes the only thing that matters. Miller was still thinking like a long-term investor in businesses, but many of his investments went bankrupt or were acquired at very low prices. In that environment, being directionally right about long-term value was not enough.

The damage was made even worse by Miller’s fund structure. As investors rushed to take money out of his fund, Miller was forced to sell positions at the worst possible time. That is what turned a bad investment environment into a collapse. His experience reinforces two hard truths. First, the risk that matters most is not volatility but permanent loss of capital. No matter how cheap you buy a business for, you will lose money if it goes bankrupt. Second, your fund structure can force you to betray your own thesis. Even if you are right over a three- to five-year horizon, client redemptions, mandates, and reputational pressure can destroy your ability to hold on long enough for the thesis to work. Miller’s fall is a reminder that brilliance in picking stocks does not insulate you from Black Swans—you should make sure you can survive even the worst disasters.

You Cannot Win the Infinite Game

The third, and perhaps most important, lesson from Miller’s redemption is that investing is an infinite game. What matters most is not chasing quick wins or building an impressive streak, but staying in the game long enough for your best decisions to thrive. One fatal mistake can end that process altogether.

Miller’s second act was not simply a lucky recovery. It reflected a change in his views on risk. After the crisis, he became more sensitive to rare events that can cause permanent impairment. He also placed greater value on managing capital on his own terms, with less vulnerability to the panic and redemptions that had magnified the 2008 collapse. That matters because independence is not just psychological. It is structural. An investor whose money can be pulled at the worst time is playing a fundamentally different game from one who can ride through distress. Buffett and Munger benefited enormously from this at Berkshire Hathaway, where insurance float gave them a durable capital base that could not be redeemed in a panic. Miller understood more clearly in his later career that controlling your investing structure is part of controlling your destiny.

His redemption also says something deeper about conviction. Miller did not abandon bold thinking after 2008. He remained capable of making large, unconventional bets when he believed the market was missing the bigger picture. His later success with bitcoin is one example. So is the fact that he continued to benefit from some of the long-duration insights that had always defined his best work. The lesson is not that he became conservative. It is that he became more aware of the difference between a misunderstood opportunity and a fragile situation where one bad scenario can wipe you out. That distinction is subtle, but it is everything. His second act suggests that the goal is not to avoid being wrong, since all investors are wrong sometimes. The goal is to avoid being wrong in a way that ends the game.

That is why Bill Miller’s career remains so useful to study. The rise shows the power of seeing businesses as complex systems rather than static financial objects. The fall shows how catastrophic risk and structural fragility can overwhelm even an extraordinary mind. The redemption shows that surviving a great mistake can deepen an investor’s understanding of risk, time horizon, and capital structure. Miller’s story is not inspiring because it is triumphant. It is valuable because it is honest. It shows that investing is not just about insight. It is also about survival.