SBC Medical - Beautiful Profits, Ugly Governance

Info

This memo was initially written around May 21st, 2025

The Pitch

SBC Medical (ticker: SBC) is a high-margin franchising machine leading the Japanese aesthetic clinic market. It’s expanding into the US and Southeast Asia, backed by a founder who owns nearly the entire company. At ~$5/share (PE of ~10x), it’s still attractively priced. But there’s one big wrinkle: the CEO’s pay package is... jaw-dropping.

What’s SBC?

SBC Medical franchises aesthetic clinics across Japan. Think Botox and hair removal—packaged with brand support, admin services, and group-buying discounts. Since going public in 2022, it’s scaled to 250+ clinics, holding strong with 40% EBITDA margins and a 70% customer return rate.

But Japan’s aesthetic market is getting crowded, and regulators aren’t exactly handing out gold stars. Clinic bankruptcies are up, and competition in major cities is heating up. Still, SBC remains profitable and is pruning underperforming units.

Growth Game Plan

Southeast Asia: Building a regional hub via its 2024 acquisition of AHH in Singapore.

US: Entered Irvine, CA with plans to grow via MedSpa M&A.

Japan: Doubling down on regional cities with comprehensive clinics, plus price hikes to offset cost pressures.

Moat Check

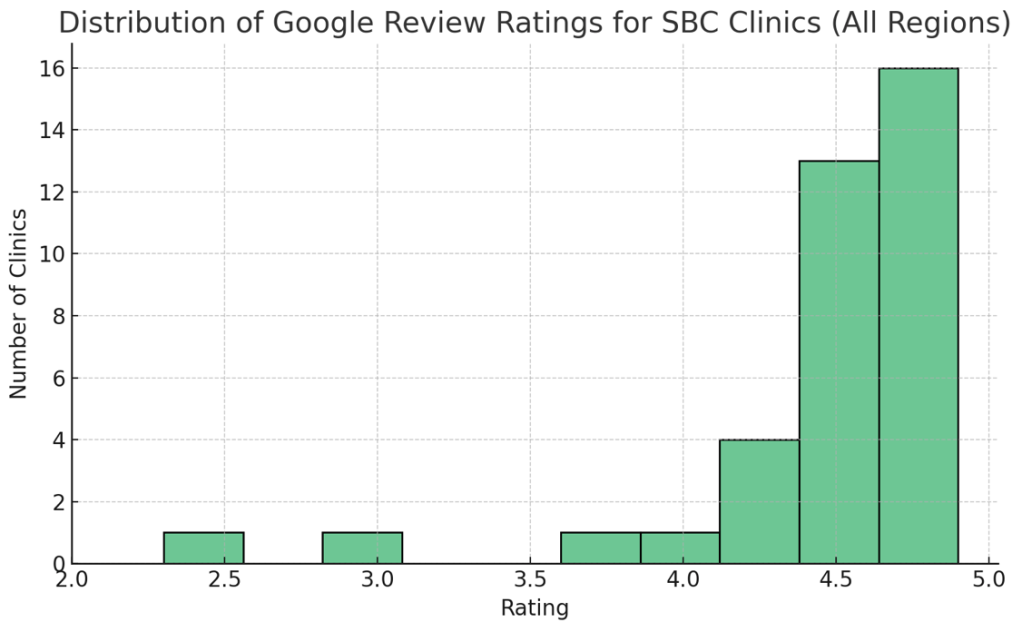

Brand Loyalty: A 70% repeat rate is no joke. It implies trust in brand value and customer mindshare. I also checked SBC clinics' google review in Japan: they're incredibly high - nearly all exceeding 4 (out of 5). As a side note, Japanese reviewers often start their evaluations at 3 stars, viewing it as a neutral or satisfactory rating. Higher ratings are reserved for experiences that significantly exceed expectations.

Scale Advantages: Bulk purchasing = cost edge.

Operational Know-How: Years of running clinics at scale is hard to replicate overnight.

Given SBC's competitive advantages (and the track record to show for it), SBC remains profitable despite headwinds in Japan and is shedding non-core operations. Importantly, if SBC can endure the pain of a down cycle, it has plenty of opportunity to consolidate and emerge as a stronger player in Japan.

Management Scorecard

Aikawa still owns ~90% of the company. That’s great for alignment—but not so great for stock liquidity.

The financials look solid: high ROIC (>30%), low debt, growing earnings.

Then there’s the comp issue. Again: $14M in 2024, $17M in 2023. Not stock. Not options. Cash. This isn’t just excessive—it’s a flashing red flag. If unchecked, it undermines the investment case entirely.

Less Beautiful Numbers

In 2024, CEO Yoshiyuki Aikawa took home $14 million in cash comp—about 3% of SBC’s entire market cap. That’s the kind of paycheck you expect from a Big Tech exec, not the boss of a micro cap business. To put it plainly: this is not just high—it’s egregious. It's more than most S&P 500 CEOs earn in cash comp. If this continues, it raises serious questions about governance.

It is difficult to speculate Aikawa's motives/philosophy around his compensation. While we know that the founder is highly aligned to how the business (and the stocks) performs, this compensation package is just too much. The worst-case scenario? Aikawa treats SBC like his personal piggy bank while minority shareholders are left holding the (empty) bag.

Capital Allocation & Risks

SBC is reinvesting—expanding aggressively abroad. Generally speaking, investors should be happy to see reinvestment given SBC's high ROIC.

But with growth comes risk:

Distraction: Managing Japan, the U.S., and SEA is a lot. We should monitor if the management loses focus moving forward.

Diworsification: New markets may not offer SBC's favorable unit economics. And we've seen SBC entering segments with poor outcomes. That said, management has shown discipline, cutting loose what doesn’t work (e.g., regenerative medicine).

Bottom Line

SBC is a bit of a mixed bag. On one hand, it’s a rare gem in the aesthetic space—40% EBITDA margins, strong brand loyalty, and undisputed market leadership in Japan. On the other hand, the CEO’s outsized cash comp is hard to ignore and raises real governance concerns.

Sources: IR presentation, Proxy Statement.

Disclaimer:

The information provided in this content is for informational and educational purposes only and should not be construed as financial or investment advice. The opinions expressed are those of the author and do not constitute a recommendation to buy or sell any securities or financial instruments. While efforts are made to ensure accuracy, the information may become outdated or incomplete over time. Investing involves risk, including the potential loss of principal. Always conduct your own research or consult with a licensed financial advisor before making any investment decisions. The author may hold positions in the securities discussed.